S

hortly after Kristy Chen and her partner, Bryce, turned 31, they quit their computer programming jobs and retired.

The couple had grown disillusioned with the “Boomers’ dream:” get a job, buy a house, be a loyal employee, retire at 65. Instead, they devoted themselves to a barebones lifestyle, saved 80% of their annual income, and amassed a portfolio of $1m — enough to live (frugally) off the dividends.

Millennials are often hounded for their poor financial management. Some 66% of 21 to 32 year-olds have no savings, and one-third don’t actively think about retirement.

But a growing subculture of young folks — mostly high-paid tech workers, like Chen — are hellbent on achieving financial independence by their early 30s.

They call themselves the “FIRE” community

Subscribers to the FIRE movement (short for “Financial Independence, Retire Early”) don’t feel like waiting around for the early bird special.

Early retirement is not a new concept. It’s been kicked around since the mid-20th century, and gained momentum during the first tech boom in the ‘90s, when books like “Your Money or Your Life,” and “The Tightwad Gazette” promoted self-reliance, frugality, and smart investing as a path to financial liberation.

In the past decade, FIRE has found a new home on the internet, fueled by gurus like Mr. Money Mustache and The Mad Fientist, who preach the gospel of financial independence through wildly popular blogs with topics like “Safety Is An Expensive Illusion” and “Luxury Is Just Another Weakness.”

Mr. Money Mustache, who retired at the age of 30 with $600k in savings, reminds his readers that “thrift is liberation, not deprivation.” He lives a spartan life in Colorado, with expenses that total just $24k per year for a family of 3. The New Yorker calls him the type of guy who “uses a woodworker’s vice to squeeze more juice out of limes.”

Mad FIentist (left), and Mr. Money Mustache (right) retired in their 30s, and now run financial independence blogs with millions of monthly readers (via MadFIentist.com)

One of the movement’s central breeding grounds, the r/FinancialIndependence subreddit, has doubled in size in the past year. Its subscribers tirelessly debate everything from “optimizing” taxes to living in a van.

Many of these fast-track retirees are tech workers under the age of 30 with healthy salaries, but the forums are also populated with nurses, janitors, teachers, and fast food employees.

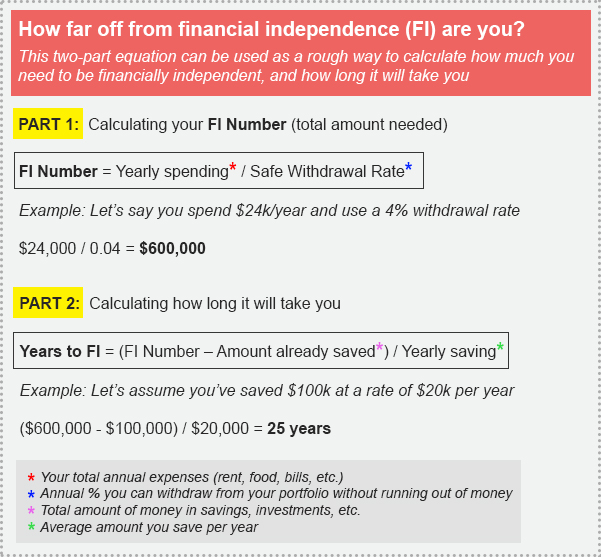

They follow financial theories like the “4% rule” (the ideal annual withdrawal rate from a retirement account without dipping into savings), and the “FI Number” (than individual’s dollar amount needed to retire).

FIRE is an innately privileged concept, but anyone can follow its unofficial formula: Dramatically minimize spending. Maximize earnings. Save enough to live off of dividends.

The young, rich, and frugal

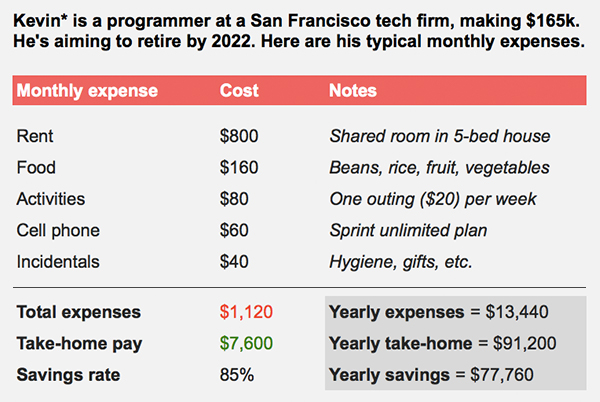

Kevin*, a 28-year-old FIRE devotee living in San Francisco, goes to extreme lengths to minimize his monthly expenses.

As a self-described “shitty coder” at a large cloud computing company, Kevin reels in a pre-tax salary of $165k per year — enough to afford him a “decent lifestyle” in one of the most expensive cities in America.

Instead, Kevin rents a shared room in a 5-bedroom house for $800 per month, sleeps on an inflatable camping mat, and eats beans and rice 5 nights a week. He relegates himself to $20 per week on social activities (going to bars, eating out), uses his company’s gym to work out for free, and gets around the city on his bicycle.

He chronicles every purchase in an Excel spreadsheet: $3.47 for a pack of floss; $8.81 for a new bike tube; $14 for a Mother’s Day gift (“Mom gets I’m on a budget,” he says).

Here’s a breakdown of his typical monthly expenses:

Over the past 4 years, Kevin has saved an average of 85% of his annual income, which he funnels into various investment accounts (a Vanguard VTSAX, an IRA, and a 401k). By saving $78k per year and averaging an 8% return, he’s accumulated $380k — about half of his $800k retirement goal.

“I’ll hit $800k by 2022, I’ll retire, and then I’ll relocate to cheaper city — maybe Minneapolis — and just live on the interest,” he says. “Prince was born there, so it can’t be too bad.”

Like many FIRE followers, Kevin doesn’t plan to stop working once he’s “retired:” he wants to pursue his true passion (playing the cello), volunteer at an inner city programming camp, and code pro-bono for nonprofits.

“For most of us, the goal of financial independence isn’t to just check out and quit life,” he says. “We just want the freedom to work on what we choose. When you take money out of the equation, you can spend your time doing more important things — for yourself and society.”

Kevin plans on pursuing his true passion (playing the cello), volunteering at inner city coding camps, and offering his services pro-bono to non-profits.

Why the rush?

Simeon*, a 25-year-old tech recruiter in Boston making $130k per year, saves 63% of her income by subsisting on $5 Little Caesars pizzas and shopping at Goodwill. “I haven’t bought a new t-shirt since, like, college,” she beams over the phone.

Like Kevin, she plans to achieve financial independence by 32 — but she’s driven by a deeper motive.

“My parents will probably never be able to retire,” she says. “My dad lost his job in the recession, and my mom is a social worker. I’ve seen them kind of struggle to get by all my life, and I think that stress is part of what makes me want to escape the traditional system.”

The extreme frugality of some FIRE millennials seems to at least be in part driven by a distrust in the economy. They were reared into the job market in the wake of a financial crisis, and have since faced declining employment opportunities, a daunting housing market, and continued wage stagnation.

All the while, they’ve been inundated with tales of impossibly young tech clairvoyants minting billions in their early 20s.

They want to escape the “shackles” of the traditional workplace and create economies of their own choosing, on their own time. Freedom, more than security, is the golden goose.

“There are certain big roadblocks to achieving financial independence, and they’re things most people want” says Diana*, a 31-year-old engineer in Seattle. “Getting an education and paying for student loans; having kids; buying a home — those are all huge setbacks. So, you have to question the very core of what you want in life. I choose freedom.”

On a sunny Saturday afternoon in Silicon Valley, I sit in on a FIRE Meetup at Stanford University.

It’s not a particularly diverse group: coders from Facebook, Google, and Symantec; marketers from Apple; a few self-styled entrepreneurs. They’re almost all in their 20s or early 30s and are at various stages in their journey toward financial independence.

We go around the circle introducing each other — name, job, title, recent “financial wins” — but a man in a down vest and loafers has something else he’d like to say.

“Work is modern-day serfdom,” he preaches, to a few approving nods, “and the only rebellion is your bank account.”

The post The 30-year-old retirees appeared first on The Hustle.

(via The Hustle)